Did You Spaccinate Yet?

Hi Everyone! 👋

Hope you’re all having a great weekend! I got back home Friday night and crossing the land border at Bellingham was quite an experience. They actually make you take an oath that you will not leave your home for 14 days or else go to jail for 3 years! So yes, I’m confined in my condo for the next two weeks. Please send food and wine, thank you.

I also got my second shot on Friday. And oh boy, did it knock me out. 5 Tylenols and many litres of water later, I’m starting to feel better now. I would still love a massage though. Maybe I should call the Covid line and request one, since I can’t leave home. But on a more serious note, if what I felt is even remotely close to how people with Covid feel, then please go get your vaccine asap.

Now onto the business of the week. Oh, I also watched Breakfast at Tiffany’s. What a delightful movie, darling! Ok, sorry back to SPACs…

As I mentioned in my last post, SPACs have been in the purgatory long enough now that the risk reward profile is starting to shift in their favor. An opportunity exists to hold a basket of high quality SPACs, with many of them still trading below NAV. A lot of you followed up from the last post about how to pick a ‘high quality sponsor’. While there is no quantitative formula to calculate what makes one sponsor better than the next, there are certain qualitative and semi-quantitative characteristics that do help with the discernment. Because ultimately when you are investing in a pre-deal SPAC, you are essentially betting on the Sponsor and his/her ability to find a good deal. It’s very much like investing in a pre-product, repeat founder, seed stage company, except you are solely betting on the founder and in some ways, relying on “past is a good indicator of future performance”. And although you don’t know exactly what company the Sponsor will merge with, their mandate and past domain experience should provide some intel into what kind of a deal to expect.

Ideally, you want to invest in a pre-deal SPAC that is -

Run by top tier operators (Chamath vs Just Another Acquisition Corp.)

Someone who has run a business themselves and has operational experience vs. just being the provider of liquidity

Just like a regular M&A, a SPAC merger should also be synergistic between the sponsors and the target. The Sponsors should add value beyond just the $$$.

With legit financial backers (PIPE investors)

Has a strong performance track record

Strong access to deal flow

And a mandate to merge with a company that is -

In the right ‘sector’ (Tech vs Industrials)

With technology that employs mostly an “asset light” business model (Fintech, edutech, healthtech vs pipeline and utilities)

Strong Underwriter (Citi, Goldman Sachs, Morgan Stanley, Credit Suisse, JPM, BofA, Barclays)

To reiterate, this is just a guideline for evaluating the Sponsor quality before a deal is announced. The bet is that it turns out to be a proxy for their skills in finding a target with -

High revenue and EBITDA growth

Wide and sustainable economic moat -

Network and scale effects

Possible regulatory tailwinds

High barriers to entry

Intangibles

Growing Total Addressable Market (TAM)

Reasonable valuation multiples (EV/EBITDA, EV/Sales)

High margin of safety

Is public ready

Overall, I do believe that Sponsors with a VC background have a better chance at succeeding than other folks. The reason is because the companies going public via SPACs are typically those late stage private companies that for the longest time chose to raise a Series Y and Series Z and remain private rather than engage in the harrowing process of filing for an IPO. And late stage VC firms were their friends. Except now, those companies can go public quickly and less harrowingly via a SPAC, and to help with that pursuit, their friends aka VC firms launched their own SPACs. Since we are talking about trading opportunities here, I won’t get into the hypocrisy of how VC firms have found a way to profit from every corner. Rather, I want to focus on the fact that given many VCs are also SPAC Sponsors, they have a natural leg up in terms of deal flow, strong relationships with founders and in-depth insight into target companies and sectors. In fact, so far I have not heard of the SEC making any noise about a Sponsor taking its own portfolio company public. Of course, it won’t be a smart thing to do as it would for sure open many cans of litigation, but on paper, it’s still permitted and not deemed as a direct conflict of interest as long as the board member closest to the target removes themselves from the negotiations.

This idea first clicked for me when I heard Brad Gerstner on the Math Money podcast. Brad runs Altimeter Capital, and they recently took Grab public via their SPAC ($AGC). Their another portfolio company Roblox also went public through an IPO recently, and he very candidly expressed that as a late stage VC, you are high up on the cap table of the company but the minute the company goes public, you lose your status and to get an even half decent allocation is a herculean task. But being a SPAC Sponsor solves that. I greatly admire Brad for his intellect but also for his candor, post this podcast.

In addition to late stage VCs, Sponsors with strong operational experience and domain expertise also make for great candidates. Take Barry Sternlicht for example. Besides being a really good looking man, Barry is the CEO of Starwood Capital Group, and has lived and breathed real estate all his professional career. He has done more deals than one can count. So for his SPAC, if he does a property or prop-tech deal, it is a no-brainer. In fact I remember when Chamath announced the $IPOB merger with Opendoor, I strongly felt that Barry should’ve led that deal with $JWS. But he is also known to not overpay.

Betsy Cohen is another outstanding Sponsor for her strong experience in the fintech domain and her extraordinary ability to get deals done. At 79 years old, she is on her 9th SPAC and killing it so far. Betsy says “You’re only as good as your last deal”; well her last one was the $FTCV merger with E-toro and I remain bullish on it in the near-to-mid-term.

Another framework that I find helpful is what Chamath said early on about the Sponsors acumen. He is getting crucified for his annual letter (that is almost six months late) because his emerging managers that he picked off of Twitter are not so good at math, but he was right in the beginning that the value-add that Sponsor brings will ultimately reflect in not only identifying the right target but also in the deal execution. For his first deal with Virgin Galactic, Chamath used the entire available time of 24 months to find it. And that is someone who has extensive experience in doing large deals. Of course it gets easier with the second one, and sometimes you can also get too overconfident before you come back to the humble equilibrium, but imagine what the Just Another Acquisition Corp Bros might be feeling right now as the clock goes tick tock tick…

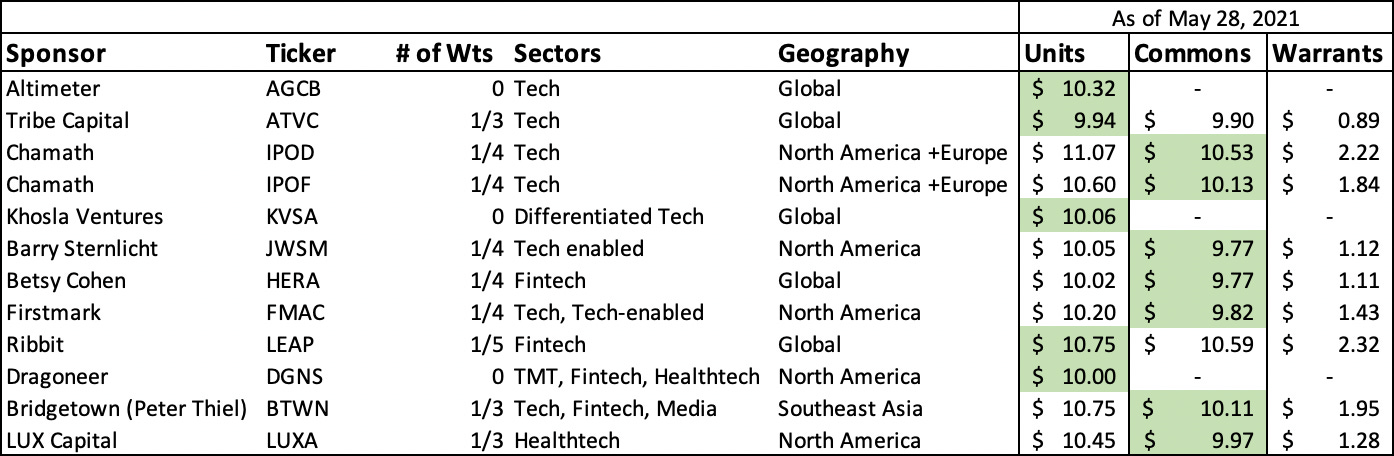

With those frameworks in mind, below is the list of names that stand out as great entry points from a risk-reward perspective. I may add more names as I see fit. The cells highlighted in green indicate which is a better buy between units and commons. Many of the names below are trading below NAV, which is basically like having your SPAC portfolio vaccinated. You will not get the SPAC virus!

There is also an opportunity in the warrants space. I read an interesting analysis recently which stated that for a SPAC that is trading at $10, the regression analysis implied that the warrants should be trading at $2.35. That warrant price compares to the current pre-announcement SPAC warrants trading at $0.81 and post-announcement SPAC warrants trading at $1.60. I haven’t dug too much into that yet but just from our list above, $ATVC, $LUX, $HERA, $JWSM and $FMAC stand out with respect to their current warrant prices. **Remember this is not trading advice, so please do your own homework guys!!**

On that note, I’ll say goodbye. Hope your week ahead is just as sunny as Phoenix :)

“Ideally, you want to invest in a pre-deal SPAC that is -

Run by top tier operators (Chamath vs Just Another Acquisition Corp.)”

LOLOLOLOLOLOLOL