SPACs - A Quarter in Review

Hi folks - wishing everyone a Happy Easter! This week we do a quick dive into how Q1 2021 shaped up for the SPAC land:

There were 298 SPACs launched in Q1 2021, raising a total of $96.3B. That one quarter number surpassed all of 2020 issuance which saw 248 SPACs raising $83.2B.

There were 24 SPAC mergers completed in Q1 with an average and a median since inception return of 31% and 19% respectively. However, looking at the returns from the all time highs that SPACs achieved in mid to late January to quarter end, the story looks a bit different. The average ATH to quarter-end return for the SPACs leaving the nest was -35% and a median return of -39%. That is more indicative of the froth that had built up in the SPAC land where every Tom, Dick and Harry SPAC was off to the moon.

We are back on earth now as the average SPAC premium has gone down from all time highs of 27% to 3.9% (vs historical average of 8.3%). The median SPAC is trading at a -1% discount.

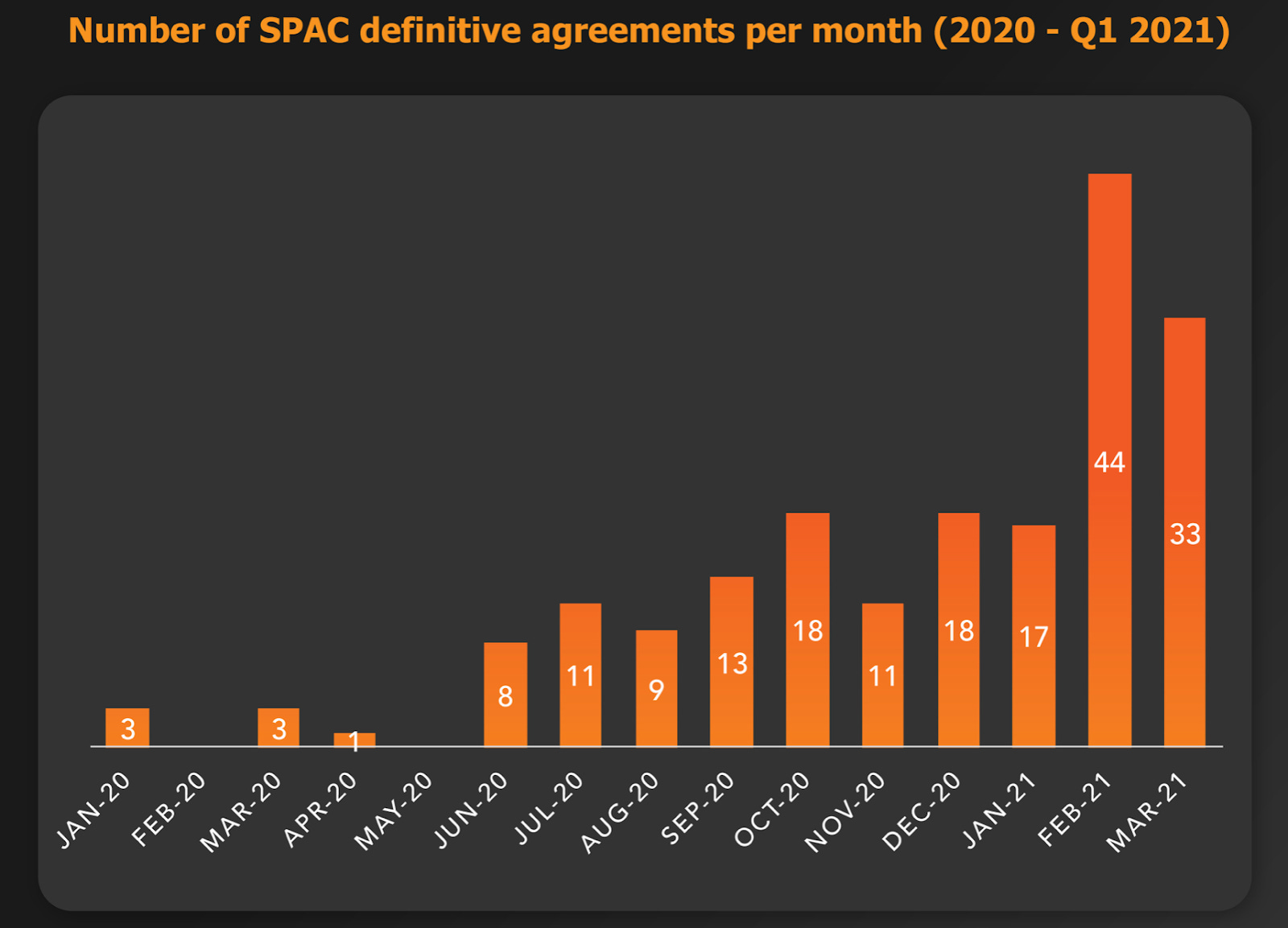

There were 94 DA’s announced in Q1, 2021 compared to 95 for the entire 2020.

The first day IPO pops have dropped.

While the pre-revenue EV and clean energy sector targets have been SPAC darlings, the reality, quite unsurprisingly so IMHO, is that they have been performance duds with most, if not all missing targets and materially lowering guidance. The best is the recent interview where Lordstown Motors CEO (NYSE: RIDE), Steve Burns literally said - “I don’t think anyone thought that we had actual orders, right? That’s just not the nature of this business." Umm… appreciate the honesty Steve, but the stock is now down 60% and there is a class action lawsuit against the company for misleading the shareholders.

This past week, albeit being a short one, was the first week with only 2 IPOs - $TWOA and $MBTC; the former trading at a discount and the latter barely keeping up at the NAV price.

On the deals side, there were 4 deal announcements. Removing the $CMII deal, the market’s reaction is neutral as if there was no deal announcement.

While both the SPAC supply tap is slowing down and the number of deals being announced are on the decline, the SPAC bears continue to remain bearish and will not settle until they see quality return to the market. Next week, we’ll discuss just that. Until then, remember that March winds and April showers bring forth May flowers!

CMLF is doing SOMA, not CMII